Aussie banks rethink credit card points, fees ahead of RBA reform

By Chris C., January 12 2017

Disclaimer

Executive Traveller may receive a commission when you apply for these credit cards via our links.

The information provided on this page is purely factual and general in nature. You should seek independent advice and consider your own personal circumstances before applying for any financial product.

Banks across Australia are reviewing their entire credit card portfolios in preparation for the Reserve Bank’s cuts to credit card ‘interchange fees’ from July 1 2017, which are shaping up to have a strong impact on credit card frequent flyer points and associated benefits.

Capping these fees at 0.8% of a transaction’s value, the changes will see many businesses paying less to process Visa and MasterCard credit card payments, along with those from ‘companion’ American Express credit cards issued by ANZ, Commonwealth Bank, NAB and Westpac.

But in turn, the banks which issue these cards to customers will earn significantly lower revenues from each transaction, meaning there’ll be less money available to the banks to spend on cardholder perks like frequent flyer points and airport lounge access.

Read: How the new RBA interchange cap will affect credit card frequent flyer points

Australian Business Traveller reveals some of the changes being considered by the nation’s major banks and how they stand to affect credit card users if implemented.

RBA cuts to credit card interchange fees: what could happen?

As banks will soon earn no extra revenue when a customer uses a companion AMEX card to pay for a purchase over a regular Visa or MasterCard, there’s little incentive for Big Four Banks to continue issuing these cards at all.

Accordingly, Westpac is seriously considering abandoning American Express companion cards entirely – or in the alternative, retaining them, but charging cardholders an additional annual fee for the privilege.

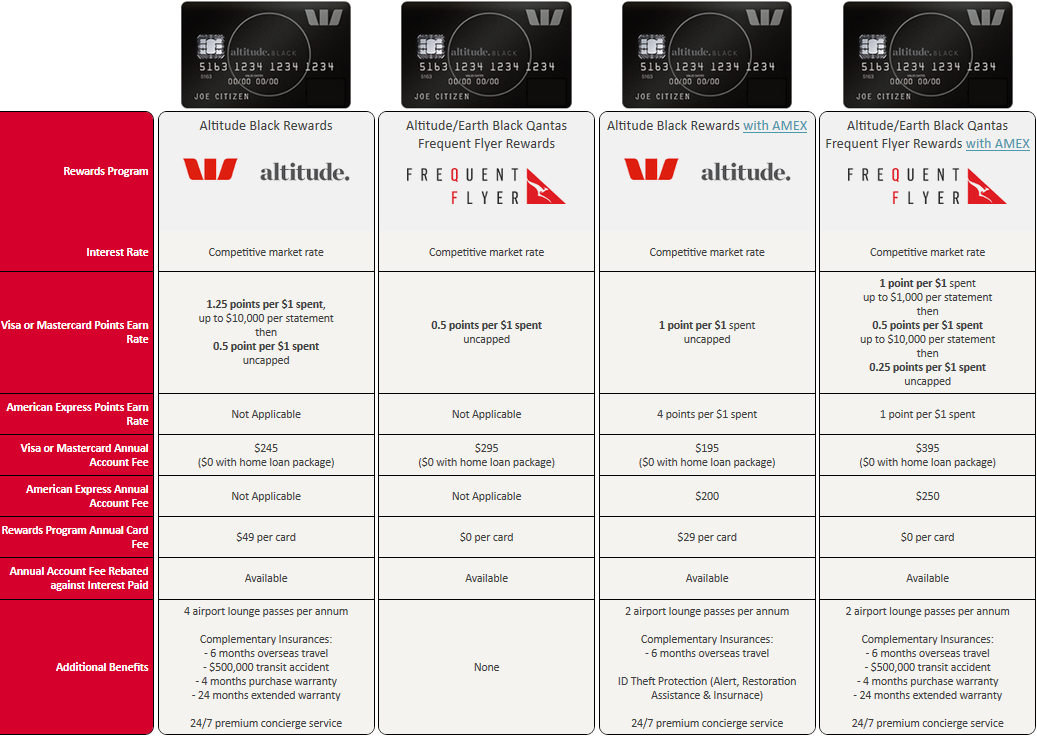

What’s more, the bank is also exploring the idea of charging a further annual 'rewards fee' per card: leaving customers to pay an annual fee for the Visa/MasterCard, a second annual fee for the AMEX, a third annual fee for rewards on one card or four annual fees to earn points on both.

Combined, cardholders could be expected to pay over $600 per year in fees for a frequent flyer-earning dual-card account, under some of the new credit card structures currently on the table at Westpac:

[Click or tap on the image above to enlarge it.]

That’s quite expensive by many people’s standards, which is why the banks have one more ace up their sleeves…

RBA credit card interchange fee cuts: switching to AMEX-issued AMEX cards

Regardless of annual cardholder fees, all bank-issued AMEX cards will be bound by the RBA’s interchange cuts – although American Express cards directly-issued by American Express Australia aren’t subjected to the same limitations.

This means that American Express can continue setting the fees that businesses pay to accept and process its own cards, earning more revenue per transaction than when a bank-issued AMEX card is used. In turn, that leaves more money available to spend on benefits like frequent flyer points for cardholders at higher earning rates than the competition.

With this in mind, Australian Business Traveller has learned that Westpac is strongly considering a new concept altogether: having American Express Australia directly-issue cards bearing the bank’s logo, but managed entirely by AMEX: similar in concept to today's David Jones American Express cards where AMEX is the direct card issuer.

Cardholders would manage their account via the AMEX website, receive their monthly statements from AMEX, remit payments to AMEX for their purchases and contact American Express Australia – not Westpac – with any transaction and customer enquiries.

Such a card would not be accompanied by a companion Visa or MasterCard but would allow cardholders to continue earning up to 1.5 airline frequent flyer points per dollar spent and with a very attractive annual fee of just $250/year, as the card wouldn't be subjected to the RBA’s interchange cuts, being directly-issued by American Express Australia.

Existing Westpac customers would merely be “introduced” to this new card and file a “shorter than normal application via American Express” upon surrendering their existing bank-issued AMEX card.

When asked to comment, a Westpac spokesperson told Australian Business Traveller that the bank "continues to look at all of its options to provide value to its customers" ahead of the RBA's looming July deadline.

RBA credit card interchange fee cuts: further changes to points and benefits

AMEX aside, it’s expected that Australian banks could offer up to 1.0 airline frequent flyer points per dollar spent on Visa and MasterCard credit cards from July, but with this figure reducing significantly after the first $1,000-$3,000 of monthly charges: plummeting earn rates thereafter to as low as 0.25 points per dollar spent.

At least one Australian bank is also looking to pare-back added benefits like travel insurance and airport lounge access, with a selection of perks included at no charge and extra benefits offered for purchase as needed.

For example, cardholders may be charged an additional $99 per year to enjoy two airport lounge visits, or could be asked to pay $79 to extend their credit card travel insurance to cover a spouse and children joining them on a trip.

Also on the table: a $29 fee to ‘waive’ all foreign transaction charges for a specific one-month period, beneficial for cardholders planning to spend more than $1,000 abroad during that window – as with a typical 3% fee, every A$1,000 spent overseas would otherwise incur $30 in added charges.

Banks are also considering bonus frequent flyer points on certain categories of spend – including direct debits, PayPal transactions, Uber and taxi charges, supermarket and department store purchases, dining expenses and public transport costs – to counter cuts to earning rates elsewhere.

What would your ideal credit card look like in the ‘post-RBA’ era? Would you happily trade perks for points to maximise your frequent flyer earnings, or would you still prefer a well-rounded card, even at a higher cost? Share your thoughts as a comment below!

Disclaimer

Executive Traveller may receive a commission when you apply for these credit cards via our links.

The information provided on this page is purely factual and general in nature. You should seek independent advice and consider your own personal circumstances before applying for any financial product.

Chris is a a former contributor to Executive Traveller.

Qantas - Qantas Frequent Flyer

25 Jan 2013

Total posts 240

In answer to your question about the ideal credit card in the 'post-RBA' era? I think a Visa with 1 point to the $ on most everyday purchases and then bonuses for supermarket/petrol/dining/transport etc. (Although some of the other insurances are quite handy).

American Airlines - AAdvantage

13 Jul 2015

Total posts 277

I think this is why I'll be sticking with AMEX issued cards directly - higher earnings (even if Westpac goes this route with Amex), and more bonus points. But that also means that Amex can increase fees ($1200 for the Platinum charge is already high, and they can go higher with more points on offer).

Qantas - Qantas Frequent Flyer

25 Jan 2013

Total posts 240

Good points. One issue I've had with American Express is over charging. When I see the Platinum charge card for $450 USD and cause we're Aussie's we have to pay worse then double that, it irritates me.

American Airlines - AAdvantage

13 Jul 2015

Total posts 277

I agree - that's just poor form, as we're being charged double.

24 Apr 2012

Total posts 2420

The standard sign-on bonus for the Platinum Charge Card is 100,000 MR Ascent Premium points in Australia (converts 1:1 to all regular airline partners and to Qantas also), not 40,000 points.

15 Feb 2013

Total posts 163

I think Jubbing is saying that in the US the sign on bonus is 40k, so the bonus here is much higher

04 May 2015

Total posts 261

I think Westpac's idea of having an Amex card issued direct by Amex is a smart move and I really hope they take that path.

The banks know that customers interested in reward points are now very familiar with Amex and know where it's accepted, and if the bank can't provide a competitive offer in terms of points and fees, customers will jump ship direct to Amex when July rolls around... especially now that Amex has the great 1.5/$1 Explorer card which basically mirrors the earn rate of each bank's top black card, and is practically free when you consider the travel credit that comes included.

The big 4 will need to create very competitive cards to compete (such as that branded Westpac card idea: $250 per year but still 1.5/$1), otherwise they'll seriously risk losing their position in the market when cardholders start switching to non-bank Amex cards to earn the points they've come to expect.

Qantas - Qantas Frequent Flyer

25 Jan 2013

Total posts 240

Just beware that your comment "...now that Amex has the great 1.5/$1 Explorer card which basically mirrors the earn rate of each bank's top black card..." may not be correct.

24 Apr 2012

Total posts 2420

Hi Jono,

That's incorrect: the AMEX Explorer card earns 2 Membership Rewards Gateway points per dollar spent, which convert to airline partners on a 4:3 basis. That gives you 1.5 airline frequent flyer points per dollar spent on all but government charges where the earn rate is lower.

(It's not a 2:1 conversion rate as with the David Jones Membership Rewards cards.)

Compared to the NAB Velocity Premium AMEX, the Explorer earn rate per dollar on everyday spend is the same, and without a points cap either.

Qantas - Qantas Frequent Flyer

25 Jan 2013

Total posts 240

Thanks Chris. Good to know as I am going through the Platinum Edge vs. Explorer card debate (on a points earn basis only) now-ish.

30 Apr 2013

Total posts 20

I like the idea of making lounges and overseas insurance as extra paid perk as long annual fee would drop a bit. Waiving FX fee for monthly bulk fee sounds good as well.

17 May 2012

Total posts 80

You still need to consider the exchange rate offered by the banks apart from the FX transaction fee. You might gain the 3% transaction fee but you might just be losing it on the currency conversion rate you receive. Its a double edged sword and not all that easy to determine which rate the banks actually use and when.

QFF

19 Sep 2013

Total posts 224

A $600 annual fee is only 1% of an annual card spend of $60k, and if we add a merchant fee of say 1% or less, then the percentage per transaction is 2% max, still below the expected award points return as per most of the figures in yesterday's tables. So I would still pay the higher bank charges. But for folks with an annual card spend of less than 20-30k, the annual fees may be too high. Would be great to have an annual bank fee based on your card spend.

Qantas - Qantas Frequent Flyer

21 Jan 2014

Total posts 336

Also what needs to be considered is claiming the annual fee as a tax deduction if you have a card used solely for business expenses, once you deduct 38% or 45% depending on your tax bracket it makes paying the annual fee a much more advantageous proposition.

VA

17 Jun 2014

Total posts 17

Appears that the only thing for sure will be increased complexity to achieve something similar to what we have today.

Virgin Australia - Velocity Rewards

07 Dec 2014

Total posts 175

So the RBA has basically screwed us over. The only winners here appear to be retailers ... call me cynical but I don't imagine they will actually pass on the savings.

Virgin Australia - Velocity Rewards

16 Dec 2015

Total posts 41

The concerning thing here is the complete lack of alignment between the RBA's intent and the outcome achieved.

05 Mar 2012

Total posts 26

Not exactly tho...because there is also the new cap on credit card surcharges which do not allow charging above cost. So at least those retailers that currently apply a surcharge would have to pass the savings on.

Virgin Australia - Velocity Rewards

09 Jun 2014

Total posts 10

I would have that that would be almost impossible to enforce?

05 Mar 2012

Total posts 26

Guess like enforcement of other consumer laws they can target the big businesses fairly easy, then if necessary, make some examples of some smaller guys. Should be sufficient to get the message out there.

Qantas - Qantas Frequent Flyer

10 Dec 2014

Total posts 58

One good thing about an Amex-issued card instead of a bank-issued one is that you'd be able to use it with Apple Pay, since 3 of the banks are currently holding out...

Turkish Airlines - Miles & Smiles

08 Jun 2014

Total posts 266

And the amazing Amex phone service you get if you need to call them. Unlike other card companies... Amex undoubteley beats them!

Qantas - Qantas Frequent Flyer

02 Nov 2014

Total posts 22

Does anyone ever do the sums on these cards. Qantas points are worth $10 per 1000 give or take. If the annual fee is $250 then at 0.5 points per $1 you have to pass $50,000 through the card just to cover the annual fee. Even if you can find a card that gives 1 point per $1 it is 25,000 points. Many cards have a limit of 3000 points per month and it is almost impossible to build up a points total significantly above the annual fee recovery.

Qantas - Qantas Frequent Flyer

27 Nov 2014

Total posts 51

If the banks withdraw from the Amex companion card business, what impact will that have on overall Amex acceptance? Will merchants rethink their Amex policy altogether when there are fewer Amex cardholders?

Qantas - Qantas Frequent Flyer

11 May 2015

Total posts 30

So i take it the banks are not content with the 20% interest charged on purchases if you're late on a payment?

05 May 2016

Total posts 620

It will be interesting to see what happens to sign up bonuses. If the earn rates for cards reduce I suspect card churning may increase.

Virgin Australia - Velocity Rewards

10 Dec 2016

Total posts 43

In the last year I have earnt in excess of 250,000 velocity points on my NAB Amex and my AMEX Velocity Platinum. I dont pay a NAB annual fee as I hold enough NAB shares (own 500 shares and you dont pay an annual credit card fee) . The Amex fee is paid by my company as its the same fee they would pay for a "company" Amex. Any smart Bank will work out that people who earn a lot of points will pay more to earn those points. All my spending is regular spending and work expenses, so I dont see an issue even if the annual fee goes up, its still value if you work the card to your advantage.

13 Jan 2017

Total posts 1

Are you sure about this 500 shares perk? I've got several thousand NAB shares, and have never had my NAB QANTAS platinum card fees waiver

Virgin Australia - Velocity Rewards

10 Dec 2016

Total posts 43

To claim the annual fee rebate there is a spending requirement for the card. It states you will get a letter with a "Shareholder Benfits Number" , however I never have, but you can contact the bank on 13 22 65 and they will process it for you. Its a bit of a clunky process but it does work. Good luck !

Hi Guest, join in the discussion on Aussie banks rethink credit card points, fees ahead of RBA reform